1031 Exchanges and Investments in REITs

Real estate investors frequently ask the question “Can I do a 1031 exchange of the relinquished property proceeds into a REIT (Real Estate Investment Trust) as replacement property?” REITs are entities that own and manage portfolios of real estate that are typically diversified by industry, geography and tenant and there are many features to REITs, including professional management, diversification and the potential for current monthly dividends and stock growth. However, an investor cannot do a 1031 exchange into shares of a REIT because the shares of a REIT are considered personal property even though the REIT, at the entity level, owns real property assets. Investors seeking 1031 exchange tax deferral must exchange property that is considered “like-kind” property which means exchanging real property held for investment or business purposes for other real property held in the same manner. REIT shares are not like-kind to real property.

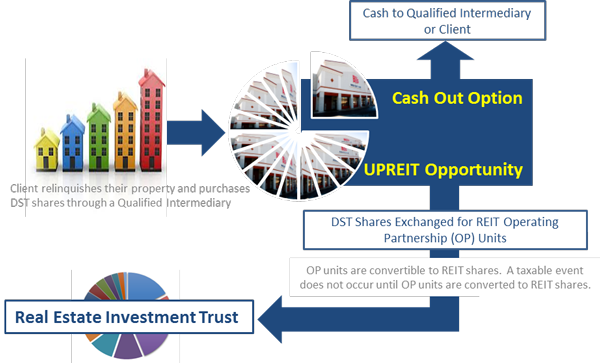

A New Replacement Property Strategy For Investors

However, although investors cannot perform a 1031 exchange into a REIT, there is a creative two-step approach that can allow investors to essentially own the equivalent of shares in a REIT.

Step #1 -1031 Exchange into a DST: An investor exchanges into a Delaware Statutory Trust (DST) that offers the potential to do an UPREIT pursuant to IRC §721 at a later point in time into operating partnership units (OP Units) in a REIT. A DST is a structure that offers fractional ownership of real property and qualifies for tax deferral. A DST has many benefits including the ability for investors to exchange out of actively managed real property and into a passive investment in a fractional ownership of institutional grade replacement property with high quality commercial tenants.

Step #2 – UPREIT from the DST into OP Units of a REIT: The investor utilizes IRC §721 and performs an UPREIT from their DST shares into operating partnership units (OP Units) in a REIT. The OP Units typically have all of the benefits as direct ownership in a REIT and are convertible into REIT shares. The UPREIT is a tax deferred transaction under IRC §721. Generally the investor is able to maintain tax deferral as long as the OP units are held. If the REIT shares are publicly traded, shares can be sold on the open market for cash. Conversion of OP units to REIT shares by the owner does create a taxable event, however, investors may choose to stagger those conversions for liquidity and tax management purposes. In addition, upon an OP Unit holder’s death, the beneficiaries of the OP Units will receive a stepped-up basis in the OP Units, similar to real estate, thereby providing greater tax planning flexibility.

For More Information on 1031 Exchanges into a DST and then a 721 UPREIT

Please contact Jason Pueschel, Managing Director of Tax Deferred Exchange Programs at Four Springs TEN31 Exchange. jpueschel@fscap.net 860-359-9129 www.fsctrust.com

Jason Pueschel is a Registered Representative of and offers securities through EDI Financial Inc., Member FINRA/SIPC, 1431 Greenway Drive, Suite 330, Irving, TX 75038, 214-528-4090. EDI Financial, Four Springs Ten31 Xchange and Asset Preservation are not affiliated.

The Surge in 1031 Exchange Activity in 2014: How Financial Advisors Can Profit

The Perfect Storm, the convergence of two large storm systems led to unusual weather conditions that ultimately resulted in the demise of the ship and its crew. In the real estate market, the convergence of much higher tax rates, a very strong commercial market, and a recovering residential market has resulted in a surge in 1031 exchange activity in 2014 – and new opportunities for financial advisors. Although real estate investors are experiencing solid gains, they are faced with a headwind of high taxation which threatens to significantly reduce investment returns. Consequently, investors are actively seeking out ways to reduce their tax liability. Once again, Section 1031 of the Internal Revenue Code has emerged as a valuable tool for boosting net investment returns by reducing tax liability, and for preserving capital for reinvestment into better performing “like-kind” replacement properties. Financial advisors can harness the opportunities provided by this “perfect storm” and help clients improvement investment returns, defer capital gain taxes, diversify and/or consolidate investments. Advisors can also help boomers near retirement who want to move from actively managed property and exchange into passive ownership such as DST or TIC fractional ownership. This article explores each of the three factors creating this “perfect storm.”

FACTOR #1: HIGHER TAX RATES

Tax rates, and their impact on an investor’s net investment return, can drive investment decisions.

Many investors are surprised to find out that today they may face four different taxes and, when combined together, the aggregate impact can result in a large tax bill owed to the government:

-

Depreciation Recapture: Depreciation recapture is taxed at 25% on all depreciation recapture.

-

Federal Capital Gain Taxes: Federal capital gain taxes are assessed on the remaining economic gain depending on an investor’s taxable income. Investors in the highest bracket pay at a 20%

rate and a 15% capital gain tax rate applies to other investors. -

Net Investment Income Tax: Pursuant to IRC Section 1411, an additional 3.8% surtax applies to

taxpayers with “net investment income” who exceed certain threshold income amounts. -

State Taxes: Investors must also pay the applicable state tax (which can be as high as 13.3%).

FACTOR #2: ROBUST COMMERCIAL MARKETS

Currently, commercial real estate (CRE) prices nationwide are about 11% above the previous market peak in 2006. International investors see the U.S. as a safe haven, and their demand further fuels CRE activity. Commercial investors have strong borrowing and buying capacity, allowing them to capitalize on favorable CRE opportunities. More evidence of the strong commercial activity can be seen by the year-to-date rent growth in the U.S. apartment market is the best since the economy started to recover from the Great Recession according to Axiometrics Inc.

FACTOR #3: RESIDENTIAL HOME PRICE RECOVERY

According to the Case-Schiller Index of 20 major cities, home prices nationwide have recovered by about

30% from the market trough The “perfect storm” resulting from the convergence of these three factors has led to an increase in 1031 exchange activity as investors turn to this powerful tax strategy to preserve investment equity and improve returns. This increase in activity has led to a significant increase in demand for financial advisors who can assess their client’s needs and suitability and then help place them in replacement property providing better investment returns. Keep in the mind that the Federal Tax Code provides numerous other ways a property owner can dispose of, exchange or sell an appreciated property and receive tax benefits. Some alternatives include Section 121, Section 453 (Installment Sale), Section 721 “UPREIT”, Section 1031 (tax deferred exchange), Section 1033 (Involuntary Conversion) and Charitable Remainder Trusts (CRT).

To learn more about these tax code sections, read Asset Preservation’s article, Selling Appreciated Property.

Congress Threatens To Eliminate 1031 Exchanges

|

|

Three separate tax reform proposals have been advanced by the House Ways and Means Committee, the Senate Finance Committee and the Treasury Department to either repeal or restrict tax deferral of gain from Section 1031 exchanges of like-kind property. Like-kind exchanges benefit millions of American investors and businesses every year. 1031 exchanges encourage businesses to expand and help keep dollars moving in the U.S. economy. |

Without the tax-deferral benefit that 1031 exchanges provide, small and medium sized businesses would not be as equipped to reinvest in their businesses, real estate values would decline, the U.S. economy would suffer, and businesses of all sizes would lose the opportunity to expand. The repeal of Section 1031 will cause a decline in real estate values as investors will be motivated to hold on to properties and to invest in more liquid, non-real estate investments with faster returns. The proposals effectively impose punitive and targeted tax increases on economically sound commercial real estate investment, the likely unintended consequence of which will be similar to implementation of 1986 tax reform modifications that resulted in a recession.

Tak Action Now!

Send a strong message to congress that 1031 exchanges are a powerful economic tool. Learn more and voice your opposition to these proposals with these critical actions at www.1031taxreform.com.

1031 Materials

1031 Materials Past

Past